ACCM4200: Statement of Advice Assignment help

Question

ACCM4200: This is a Kaplan Business School Assignment for the Advanced Financial Accounting course in which the student is required to imagine themselves in the role of a manager working for Key Business Services, which is a consulting and accounting company that counsels clients on accounting matters, such as implementing the Australian Accounting Standards. It has been remarked that on behalf of the company’s directors, the student has been asked to draft a Statement of Advice for Flummoxed Limited that addresses the several accounting concerns that are brought up in a letter provided along with the task file.

Solution

Students all across Sydney face difficulty in doing this assignment, as it demands a comprehensive knowledge of various advanced-level financial accounting concepts and theories. This is why they require Master of Professional Accounting Assignment Help from top subject matter experts. We take pride in delivering the best quality solutions at affordable prices. In this assignment solution, a thoroughly written Statement of Advice has been developed by our experts addressing various accounting issues related to Flummoxed Limited highlighted in the letter brought up by Ms. Lex.

Statement of Advice

As per the structure taught to the student through the course modules, our experts have developed a well-written statement of Advice that begins by addressing the concerned stakeholders.

XXXX,

Manager

Key Business Services

1 Main Street,

Melbourne, 1000

5 June 2023

Purp Lex,

PA to Managing Director,

Flummoxed Limited,

201, Main Street,

Business District,

Melbourne, 1000

Dear Mr. Lex,

This statement of advice has been issued in response to your letter dated 29 May 2023. The accounting issues faced by your concern were raised in this letter.

If you want to buy Advanced Financial Accounting Assignment Help in Australia, WhatsApp us at +447700174710 today!

Issue 1

Firstly, it has been suggested that Flummoxed Limited must adhere to the Research and development cost guidelines to accurately reflect its financial position and performance. In providing a rationale for this issue, our experts have clarified how to decide which research and development expenses should be capitalized and which should be expensed. Journal entries have also been included and our experts have also provided examples of the requirements that apply to Flummoxed Limited. This is how we provide the best Financial Accounting assignment help in Sydney.

Identification of the Issue

In the given situation, Flummoxed Limited requires advice if the expenditure made on research and development of a new digital learning device must be treated as an expense or recognized as an asset in the financial statements of the company

Identification of Australian Accounting Standard

The intangible asset refers to those assets which do not have any physical existence as per AASB 138. Paragraph 21 of AASB 138 further explains that the events of the past give the entity control over these assets. It is also evident that the economic benefits from the asset would flow to the entity in the future period and the cost of the asset could be measured reliably (Australian Accounting Standards Board, 2015). Paragraph 22 AASB 138 states that the flow of the economic resources to the entity would be made based on the manager’s best estimate of the expected set of economic conditions which would be present during the useful life of the intangible asset.

Paragraph 51 of AASB 138 explains that if an intangible asset is generated internally, sometimes it is difficult to determine if it would be recognized as an asset in the financial statements due to two issues –

The challenges in identifying if the intangible asset would generate economic resources for the entity in the future period and since when will the generation of the economic resources begin,

The entity is unable to measure the cost of the asset.

Recommendations and Explanations

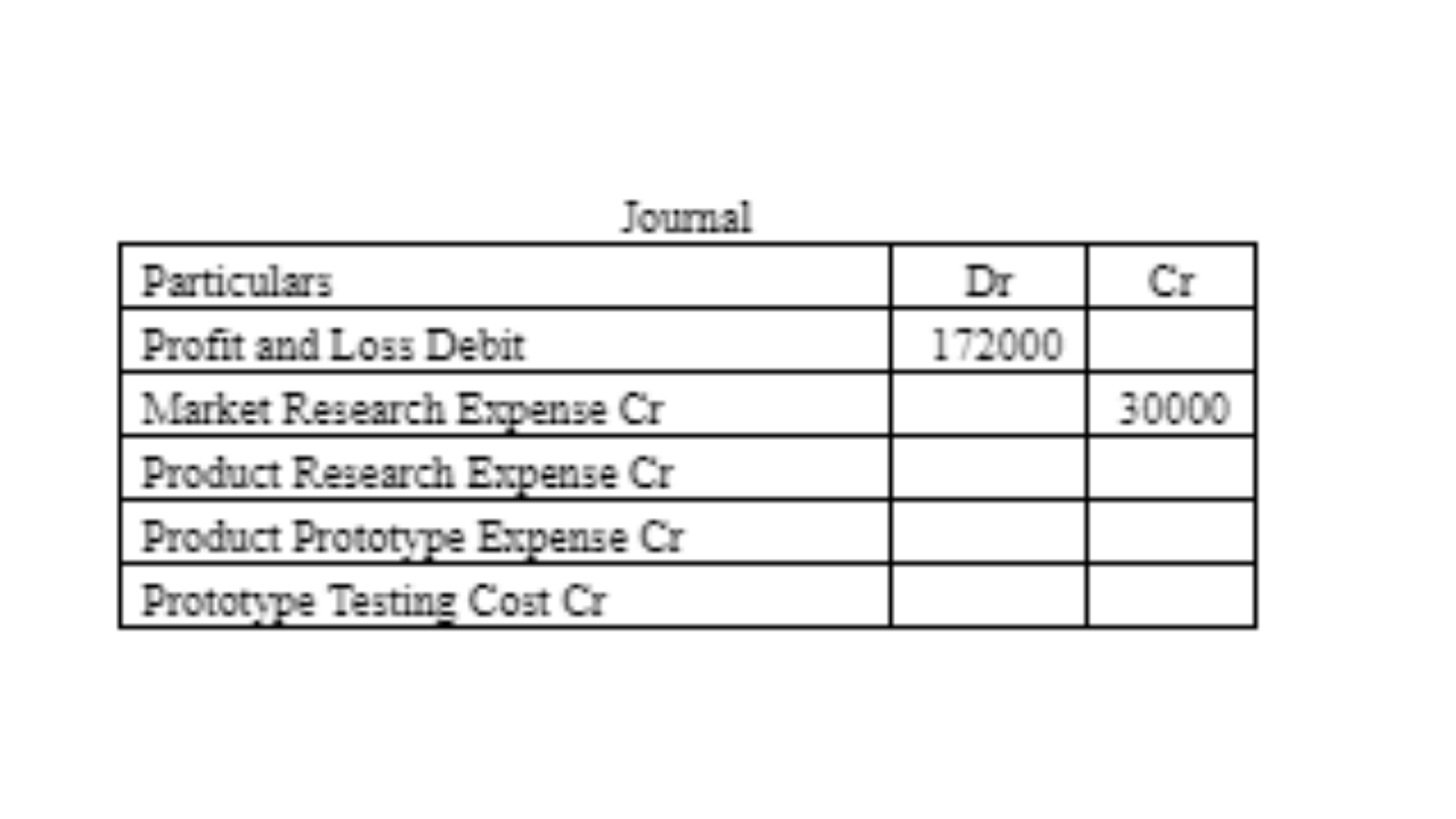

The company invested in the development of a new digital learning device that could be recognized as an intangible asset (upon meeting all the criteria) since it does not have a physical existence. The company spent $30000 to understand the needs of the potential users and $40000 to determine the suitability of the material for the device. Both these expenditures would be considered as expenditures made in the research phase since till this stage there is no certainty of the creation of the new asset and the possibility of flow of economic resources to the entity is also minimal.

Journal

Get KBS assignment help in Australia at discounted prices. It’s our seasonal discount season. Please approach us for ACCM4200 assignment help. Call us today at +61 871501720.

Issue 2

The following section addresses the second issue for Flummoxed Limited. An ex-employee sued Flummoxed Limited for workplace injury, for which the court ruled in the employee’s favor due to safety non-compliance, pending damages determination. The statement of advice recognizes this potential liability or provision in financial statements. Our experts have responded to each director’s point of view, while providing a thorough explanation of the proper accounting treatment.

Identification of the Issue

In this case, the company is facing litigation charges from an ex-employee who was injured at the workplace.

Identification of Australian Accounting Standard

Paragraph 14 AASB 137 explains the provision as a present obligation of the entity which arises from past events. The company will probably witness an outflow of the economic resources for settling the liability and the amount of economic outflow could be estimated reliably. However, the timing and amount of the liability are uncertain as explained in Paragraph 10 (Australian Accounting Standards Board, 2018).

Recommendations and Explanations

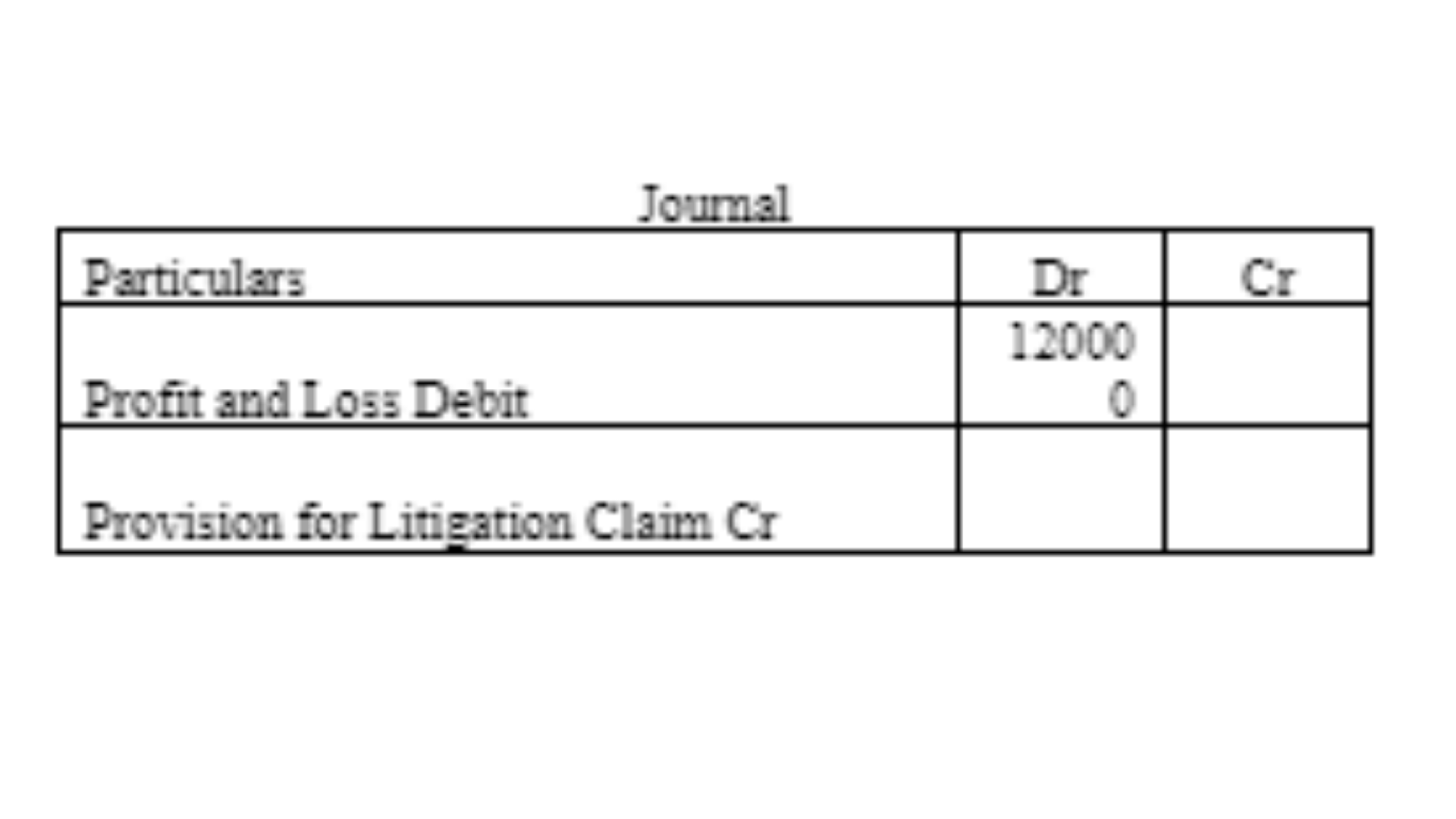

In this case, the court has already determined that the negligence was from the company and the company has to pay for the damages. Since the financial obligation has already arisen, therefore it could be treated as a provision. Even if the amount and timing of the obligation is not certain, the outflow of the economic resources is certain therefore, the contention of the third director of not recognizing this event at all in the financial statements is incorrect. The liability of the company has arisen, but the amount of liability is not certain and the court has not yet issued any notice to pay any sum to the ex-employee.

Journal

Looking to get Master of Professional Accounting Assignment Help from Ph.D. experts? Let us help you. Reach out today- onlineassignmentservices1@gmail.com.

Issue 3

Lastly, it has been highlighted that the company as a guarantor for its subsidiary’s loan, faces potential risk due to the subsidiary’s financial challenges. While the subsidiary may struggle to repay the loan, its net assets suggest a likelihood of meeting obligations through asset liquidation. In providing ACCM4200 Statement of Advice Assignment help, our experts have provided a careful consideration of potential impacts on both companies’ financial health and obligations.

Identification of the Issue

In the given case, the company has acted as a guarantor for a loan that has been taken by one of its subsidiaries.

Identification of Australian Accounting Standard

Paragraph 10 AASB 137 defines contingent liability as a present obligation that may arise on the happening or non-happening of a certain event (Australian Accounting Standards Board, 2018). The contingent liability is not a liability as it is not evident that it will result in an outflow of the economic resources of the entity and so, it must not be recognized in the financial statements. Paragraph 13 AASB 137 explains that the contingent liabilities are not recognized as a liability because do not exist on the reporting date and they do not meet the recognition criteria as it is not certain if these liabilities would result in outflow of the economic resources.

Recommendations and Explanations

In the given case, the subsidiary company is facing financial difficulties but it is still a going concern and it is operational. So, the liability from the guarantee has not yet arisen for the company so, it is still a contingent liability for the company. It would occur only if the subsidiary company is unable to repay its debt. The company does not require to recognize it in its financial statements.

This is only a snippet of the complete Statement of Advice written by our experts. If you want to know more, you can get Kaplan Business School Assignment Help at flat 30% off! WhatsApp us at +447700174710 today!

Conclusion

This Statement of Advice lastly presents a concluding remark of all the suggestions proposed by our experts above. You can read half of this conclusion below:

The statement of advice presented above presented a detailed description of each issue including the major challenges which were being faced in each issue.

Order Financial Accounting assignment help in Sydney from the best subject matter experts! Give us a call at +61 871501720.